Our Blogs

A Cactus Approach to Investing

I am not a master gardener but if I had to take care of a plant, I would pick a cactus. I would choose one that just needed to be planted and left alone. Index funds are the cacti of the investment world. Sure, the initial set up takes a bit of work, but once you get that done, you can basically forget about it.

Those with green thumbs might question why I would want a plant at all if I’m not willing to put in any effort. Well, I also like eating tiramisu and don’t know how to make it. Similarly, not knowing the difference between long-term debt and non-current liabilities isn’t a reason to avoid growing my money. This is where index funds come in.

Here’s a basic overview of the difference between a mutual fund and an index fund:

| Mutal Fund | Index Fund | |

| What is it | An actively managed fund that invests in companies on specific criteria | A passively managed fund that invests in companies to mimic the market index |

| Management | Fund manager | Computer |

| Expense Ratio | ~0.5-2.5% | ~<0.3% |

| Returns | Dependent on the fund manager’s insights | Independent of the provider;simply follows the market index |

*Note:It is statistically impossibe for a fund manager to continually beat the market over 20-30 years

Warren Buffet is famous for his ‘buy-and-hold’ strategy of investing—he invests in a company and holds on to his investment for decades. This is in direct opposition to a typical fund manager’s approach, which involves continuously moving investments to companies likely to yield high returns. The very act of continuous movement incurs transaction costs and capital gains taxes that can eat into your money over time. In addition, mutual funds cost more because they rely on the expertise of the fund managers and yet, except for a few Phelps-like investors , the vast majority of them cannot beat the market in the long run. By investing in index funds, I can sidestep the ‘wisdom’ of man and leave it to the markets.

‘In 2007, Warren Buffet made a now legendary bet with hedge fund managers, Protégé Partners. Buffet put $1 million at stake betting that his choice of a low-cost index fund would beat the cumulative net returns generated by Protégé Partners’ hedge funds over a period of 10 years. At the close of the bet, Buffet’s index fund had a compounded 7.1% annual return, compared to Protégé’s 2.2%.’

There is also the idea that if I (or a fund manager) can find the right company to invest in now, a small investment will be enough to retire on. For instance, if someone used ₹10,000 to buy 100 shares in Wipro in 1980, those shares would be worth several hundred crores today due to bonuses and stock splits over the years. It’s fun to imagine having such foresight in retrospect, but in reality, few of us can achieve this. Instead, I can invest in the market as a whole through index funds and trust that companies like Wipro will drive up the value of my investment anyway. (Incidentally, Wipro is on the Indian indices today).

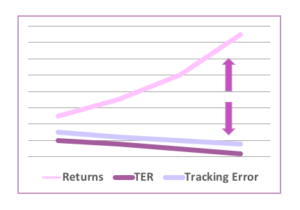

As index fund investments are computerised, there isn’t a lot of variation in the offerings from different providers. The two main criteria I used are expense ratio and tracking error. The expense ratio determines how much of the money you invest is spent on fees. It would seem logical that the lower the TER (total expense ratio), the higher the earnings. However, the devil is in the detail. The difference between a TER of 0.1% and 0.14% appears negligible, but over time and with compounding, it will matter. It’s also important to choose ‘direct’ over ‘regular’ funds to further lower the TER. The other important factor to consider is tracking error, which determines how closely a fund mimics the actual index. Since the idea is to follow the index, the lower it is, the better.

The lower the TER and the tracking error, the higher the returns

I use Zerodha to invest, but it may not be the easiest system to start with. ET Money and Groww have much more user-friendly sites, and both allow you to explore all their options without signing up.

Choosing an index fund and provider isn’t the end of my investment process. I still have to plan how much and at what frequency I am willing to invest. I also have to look at eventually diversifying my investments to balance risk and savings for short term-goals. And simply because the ‘cactus approach’ is my main strategy, I will also need to automate these steps for the future. All of this and more in my upcoming blog posts—stay tuned!

The multitude of options and decisions can be, and often are, overwhelming initially, but taking one step at a time makes it all doable. And, more importantly, many of them are only difficult at the beginning.

Millennials are famous for their ‘succulent mania’ because of the low effort required to maintain these plants. Assuming I still want to be able to buy tiramisu when I retire, it makes sense to start planting my low-effort cacti/investments as soon as possible.

One comment on “A Cactus Approach to Investing”

Comments are closed.

Suggested Blogs

Love at First Sight: Cubbon Park

I am not a master gardener but if I had to take care of a plant, I would pick a cactus

Kanika Tekriwal of JetSetGo

I am not a master gardener but if I had to take care of a plant, I would pick a cactus

Between a Stock and a Hard Place

I am not a master gardener but if I had to take care of a plant, I would pick a cactus

Get in touch with us

Be the first to hear about our upcoming programs

Interesting….. got me thinking….. towards action… thanks.